For a first or second investment house, as well as for developers pursuing rental projects in the 12- to 24-unit range, the CMHC Halifax Rental Market Report (2025–2026) provides a critical lens through which to understand the current state of the Halifax CMA. While the broader narrative surrounding the market points to rising vacancy in certain segments and a substantial pipeline of new construction, the report reveals a more segmented and nuanced reality. For smaller investors and early-stage investment houses, this is not a signal to step back, but rather a call to operate with greater precision.

A first or second investment house typically approaches the market differently than large institutional developers. Capital is more limited, risk tolerance is more carefully managed, and project selection must be deliberate. These investors are not positioned to absorb long lease-up periods or large-scale execution risks. In contrast, developers working on 12- to 24-unit buildings benefit from a scale that is both manageable and flexible. Importantly, this scale also aligns with more accessible financing structures, including CMHC-insured programs, where requirements are often less stringent for smaller projects compared to larger, multi-phase developments.

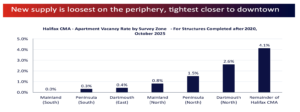

This structural advantage becomes particularly meaningful when interpreting the findings of the CMHC Halifax Rental Market Report (2025–2026). One of the report’s clearest conclusions is that vacancy is not evenly distributed across the market. It remains tight in central and established areas while loosening on the periphery. For large developers delivering hundreds of units in expansion zones, this may present a growing concern. For first or second investment houses and small-scale developers, however, it presents an opportunity.

Smaller projects are not tied to large land assemblies or major suburban expansions. They can target infill locations, underutilized parcels, and neighborhoods where demand is stable and deeply rooted. In these areas, vacancy remains structurally lower, and absorption is more predictable. The implication is clear: while the broader market may show signs of adjustment, the segments most relevant to smaller investors remain resilient.

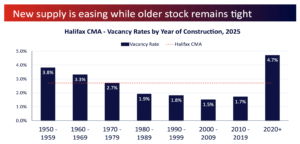

The report also highlights a divergence between new and older rental stock, with newer buildings experiencing higher vacancy rates. This is largely a function of pricing. New developments are entering the market at elevated rent levels, which are increasingly constrained by affordability limits.

For a first or second investment house, this reinforces the importance of disciplined positioning. These investors cannot afford to misprice their product or overbuild. Similarly, developers in the 12- to 24-unit range benefit from focusing on efficiency rather than excess. Their strength lies in delivering functional, well-designed units at rent levels that remain accessible to a broader tenant base. They are not competing with luxury towers; they are serving the segment of the market where demand is deepest.

This is further supported by one of the most important findings in the CMHC Halifax Rental Market Report (2025–2026): the most affordable rental units remain the most constrained. Vacancy is lowest at the lower end of the rent spectrum, indicating sustained and unmet demand. For smaller investors, this is not just a data point, it is a strategic direction. It highlights where stability lies and where long-term occupancy is most reliable.

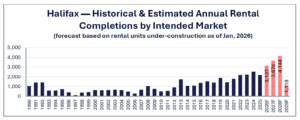

The construction pipeline must also be understood in context. The report identifies over 12,700 rental units currently under construction across Halifax. At face value, this may appear to signal saturation. However, the composition of this pipeline is heavily skewed toward larger developments, particularly those in the 50- to 199-unit range and above.

This distinction is critical. A first or second investment house, or a developer building 12 to 24 units, is not directly competing with this supply. The market is receiving large increments of housing, but relatively little small-scale, incremental development. This creates a structural gap. While institutional capital dominates large projects, smaller-scale opportunities remain comparatively underdeveloped and less competitive.

Execution risk further differentiates these two segments. The Rental Market Report notes that more than 600 units are already overdue in the current construction pipeline. Large projects are inherently more exposed to delays, cost overruns, and financing pressures. In contrast, a 12- to 24-unit project is simpler to manage, faster to deliver, and less vulnerable to external disruptions.

For a first or second investment house, this reduction in execution risk is essential. It allows capital to be deployed more efficiently and reduces the likelihood of prolonged exposure to unfavorable market conditions. At the same time, CMHC financing structures tend to be more accessible for smaller projects, with less complex underwriting requirements compared to large, institutional-scale developments. This further enhances the feasibility of smaller projects in the current environment.

The report also highlights that more than 3,300 residential units have been approved but not yet started. This reflects a level of hesitation in the market. Rising costs, financing constraints, and uncertainty around future rent levels are causing delays. For smaller investors and developers, this hesitation creates opportunity. With fewer projects advancing in the near term, competition is reduced, allowing well-positioned smaller projects to capture demand more effectively.

Ultimately, the report does not point to a declining market. It points to a market that is recalibrating. The softening observed is concentrated in specific segments, particularly higher-priced, newly delivered supply. It does not reflect a broad weakening of demand. On the contrary, demand remains strong where affordability and location intersect.

For first and second investment houses, as well as developers operating in the 12- to 24-unit range, the implications are clear. This is not a market that rewards scale alone. It rewards discipline, selectivity, and alignment with real demand.

A well-located, well-priced small project can outperform larger developments by achieving faster lease-up, lower vacancy, and more stable long-term returns. The advantage lies not in building more, but in building smarter.

Halifax remains a good rental market. But today, success belongs to those who understand its segmentation, leverage their scale appropriately, and position themselves where demand remains strongest.